Executive Summary

In an economically fragile environment, combined with the need to innovate fast and efficiently, community association management companies face a narrowing window of opportunity to secure their financial health. An economic slowdown is brewing alongside rising consumer delinquencies, threatening to squeeze HOA/COA budgets. Delinquency trends on credit cards and mortgages are climbing back toward or above pre-pandemic norms, and major lenders are already bracing for losses.

In this environment, recovering overdue assessments now is urgent. It represents recallable revenue that can strengthen your budget before wider financial stress hits. This fall’s budget planning cycle is effectively the “last chance” to integrate Accounts Receivable (AR) recovery strategies before delinquencies potentially worsen into 2026.

By proactively recouping what is owed, associations can shore up reserves and avoid desperate measures later, like slashing services or levying special assessments.

Acting now on AR recovery is a high-impact, low-friction way to stabilize community finances ahead of tougher times. The window is closing, but it’s not shut just yet.

Remember: once homeowners fall further behind, those dollars become exponentially harder to collect.

Economic Outlook & Consumer Stress Signals

We can’t wave a magic wand and predict a recession, but we can look at the facts: Multiple economic indicators are flashing warning signs of consumer financial stress, which in turn foreshadow higher AR risks for HOAs/COAs. While there are positive signs for an economic turnaround, a struggling labor market and sharp rise in debt needs to be top of mind for management company executives.

Credit-card delinquencies are rising sharply.

After an anomalously low period during 2020-2021, credit card late payment rates have rebounded to or above pre-COVID levels. As of mid-2025, the average credit card delinquency rate hit 2.8%, higher than in June 2019 before the pandemic. U.S. card delinquencies are also at their highest level in five years, erasing the pandemic-era improvement. Major card issuers see trouble brewing: banks like JPMorgan Chase and Citigroup have been bolstering their loan loss reserves by billions in anticipation of consumers falling behind.

Household debt loads have surged to decade highs.

U.S. consumers are now carrying record levels of debt, including rapidly growing credit card balances. Adjusted for inflation, the average credit-card balance per household now exceeds $10,000 – a threshold last seen around 2009. Total credit card debt hit $1.29 trillion in late 2024, an all-time high in nominal terms.

“Credit-score hangover” is hitting subprime borrowers.

During the pandemic, many Americans’ credit scores actually improved thanks to stimulus and forbearances. Now that effect has waned – average credit scores have begun to dip for the first time in a decade – and those with shakier credit are rapidly losing ground. Nonprime consumers’ credit scores have fallen below pre-pandemic levels as they accumulate debt and face inflation pressures. Even more troubling, these borrowers’ delinquency rates on credit cards and auto loans jumped about 28% in the past year, reaching the highest point since the aftermath of the Great Recession. The segment of homeowners most likely to struggle – those with lower credit or incomes – is entering 2026 in a significantly more precarious financial state. This reduced payment capacity in a swath of the population will inevitably translate to higher HOA delinquency rates absent intervention.

Housing Market Distress: Delinquencies & Foreclosures Are Climbing

The housing sector is not immune to these pressures. Mortgage delinquencies and foreclosure actions have begun creeping upward, indicating stress even among homeowners (the very demographic comprising HOAs).

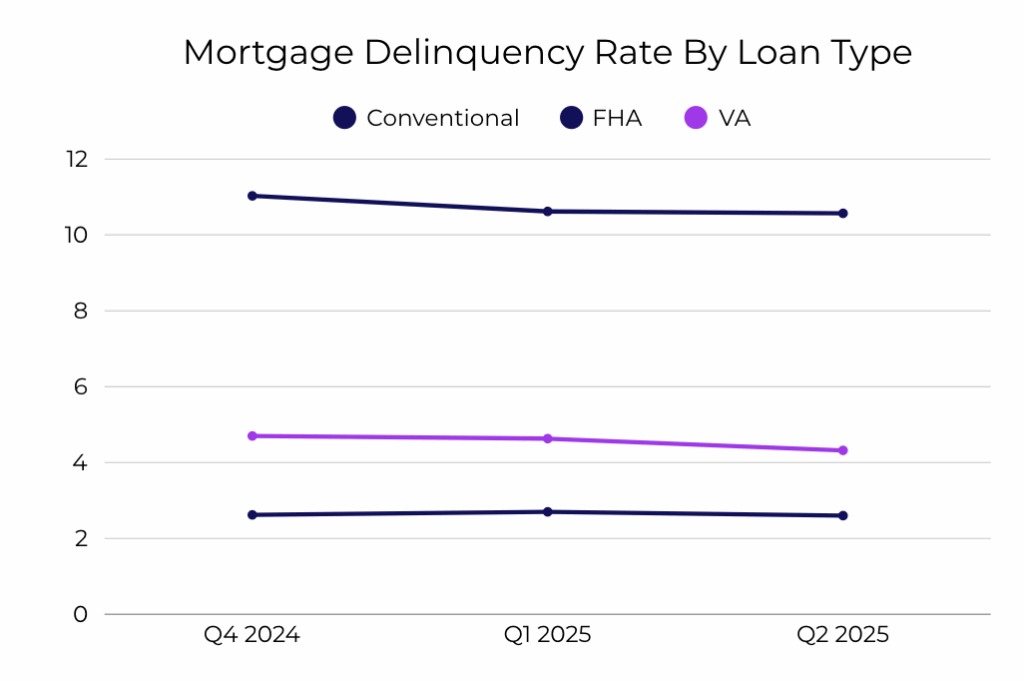

Mortgage delinquencies ticked up to 4.04%

By Q1 2025, 4.04% of mortgage loans were delinquent, a slight increase (+10 basis points year-on-year) and the first notable rise after a long period of improvement. While still low by historical standards, this uptick suggests more homeowners are missing payments. Notably, the increase was driven by conventional loans – those without government backing – as some borrowers came off pandemic-era savings and faced higher living costs.

Foreclosure start rates also rose in early 2025: about 0.20% of all loans entered foreclosure during Q1, up from 0.15% at the end of 2024. In other words, banks initiated roughly one foreclosure for every 500 mortgages – a small share, but the largest volume of new foreclosures in years.

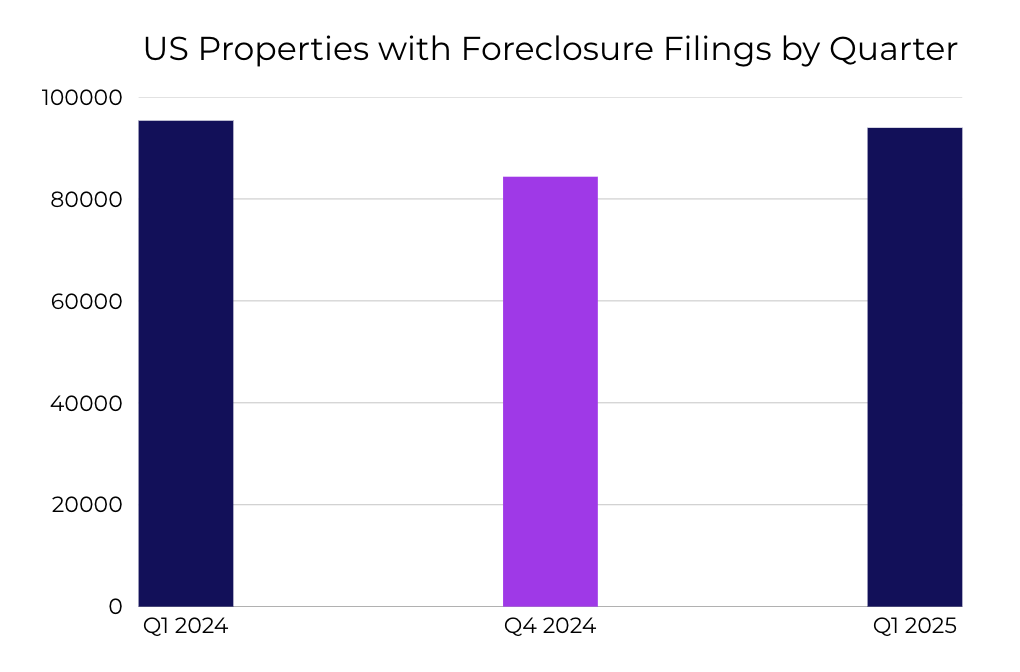

Foreclosure filings jumped 11% in Q1 2025 (QoQ).

According to ATTOM Data, 93,953 U.S. properties had foreclosure filings in the first quarter of 2025, an 11% increase from the prior quarter. The spike ended three consecutive quarters of decline in foreclosures, hinting that lenders are ramping up enforcement as forbearances and borrower cushions dry up.

New foreclosure starts totaled 68,794 in Q1, up 14% from Q4 2024 (and 2% above the year-ago level). March 2025 alone saw over 35,000 foreclosure filings, an 11% monthly increase. While overall foreclosure activity remains well below mid-2000s crisis levels, the quarterly growth is a clear sign of building strain.

FHA loan delinquencies hover close to 11%.

Perhaps most relevant to HOAs, the delinquency rate on FHA-backed mortgages has soared into double digits. FHA loans – which cater to first-time and lower-income buyers with small down payments – had a seasonally adjusted delinquency rate of ~10.6% in Q1 2025, roughly 11% when rounded. This marks the highest FHA delinquency level since 2013. This is especially concerning because FHA borrowers overlap closely with HOA demographics – they often purchase condos or starter homes in associations. Many are younger owners or those with limited financial cushion.

FHA and VA delinquencies have become the “canaries in the coal mine” for housing in this cycle. Boards and managers should take note: an FHA delinquency spike implies that a wave of first-time homebuyers in HOAs are struggling.

Why 2025 Is The Final Anchor Point

Given the economic trends, Fall 2025 represents a critical “now or never” moment for HOAs/COAs and their respective management companies to fortify their finances. This period – late Q3 into Q4 – is when most associations finalize budgets for the next fiscal year. It may be the last realistic chance to implement AR recovery measures before economic conditions potentially worsen. Here’s why timing is so crucial:

1. Budget planning sets the tone for 2026. Once your 2026 budget is approved (by late fall), you lock in assumptions about revenue and expenses. If you do not build in an aggressive AR recovery plan now, you’ll be relying on optimistic collection assumptions next year just as delinquencies could spike. Essentially, failing to act now means gambling that owners who are already late will somehow catch up – a bet at odds with the economic outlook. Instead, by integrating an AR recovery program into this budget cycle, you can bake in realistic collection targets and perhaps even new income streams (e.g. late fee recoveries) to offset rising costs.

2. The longer you wait, the harder it gets to collect. Delinquent HOA/COA assessments tend to age like milk, not wine; they get worse, not better, over time. A homeowner 30 days behind might be salvageable with a payment plan; a homeowner 18 months behind (and maybe in pre-foreclosure) is a much tougher recovery. If economists are right that consumer finances will deteriorate into 2026, then arrears that exist today will only deepen, and new delinquencies will mount. Simply put, waiting even 6 or 12 months will shrink the pool of collectible receivables as some accounts go to third-party collections or bankruptcy. This fall is likely the high-water mark in collectability before a potential recession. Boards should seize this moment to chase every last dollar of 2023–2025 delinquencies now, while more owners still have jobs, side incomes, or savings to draw on.

3. Mid-year crises are costly and disruptive. Consider the alternative scenario: a management company ignores the warning signs, and by mid-2026 they find that 10–15% of owners are delinquent. Now the HOA is facing cash flow shortfalls – reserves being drained to cover operations. In such a pinch, boards often resort to emergency special assessments, cutting services and amenities, or increasing assessments on the paying homeowners. These reactive moves can damage homeowner relations and even property values. We’ve seen cases where HOA boards in crisis end up imposing large special assessments to fill budget holes – a move that ironically can cause further delinquencies. By contrast, recovering AR proactively in fall 2025 can prevent those nightmare scenarios. It’s far better to have extra cash on hand (collected from those who owe it) than to beg your membership for a bailout later.

4. Getting ahead of third-party collections. If delinquent accounts are not cured in-house, eventually many will be turned over to outside collection agencies or attorneys. But once a third party steps in, the dynamics change: homeowners often dig in as fees and interest balloon, and the HOA/COA typically recoups far less (after collection fees) or waits until a lien is enforced or foreclosure resolved, which could be years. In other words, once it goes external, that debt is largely “dead” to your budget. By acting now with a pre-collections recovery strategy, management companies keep the process within the HOA/COA’s control and capture funds before they get absorbed by collection costs. Think of Fall 2025 as the deadline to “kill off” the need for outside collections in 2026. The goal should be that by next year, no account is so far gone that it has to be handed to a collection agency. That’s achievable if you start the recovery push today.

AR Recovery as High-Impact, Low-Friction Revenue

Why focus on AR recovery as the solution? Because it represents perhaps the highest-impact, lowest-friction source of revenue available to HOAs/COAs and management companies right now. Unlike raising assessments (which angers homeowners) or cutting maintenance (which erodes property values), improving AR recovery is a win-win: it returns money already owed to the community and can even generate new income for management.

1. Recapture of lost funds. Every dollar in overdue fees that you recover is a dollar added back to the budget. These funds can plug reserve gaps, pay for delayed repairs, or simply improve the HOA’s fiscal cushion. It’s far easier to collect an existing receivable than to seek new revenue streams. Many associations are sitting on significant AR balances that are essentially “low-hanging fruit.” Harvesting that fruit now has an immediate budgetary impact.

2. Revenue boost for management companies. AR recovery can also create a modest revenue stream for management firms. By capturing fees or retained late charges that would otherwise be lost, a well-run program can add about $3.60 per door annually—over $18,000 a year for 5,000 doors. Unlike raising management fees, this is low-friction income because it comes from funds already assessed, not new homeowner charges.

3. “Found” money versus new fees. AR recovery taps into revenue already owed, not new charges. Instead of burdening all homeowners with higher dues or special assessments, it ensures fairness—everyone pays their share—while restoring equity in the community.

Data-Driven Strategy Essentials

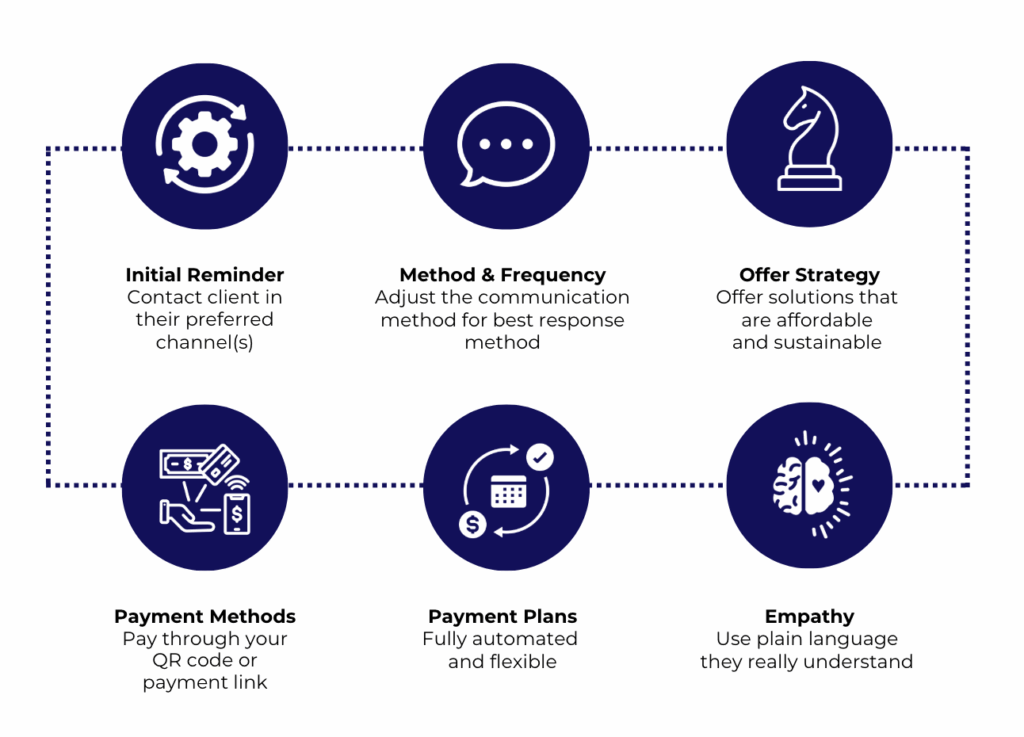

To execute AR recovery effectively (and efficiently), HOAs and management companies should leverage a data-driven, technology-enabled strategy. Gone are the days of blanket demand letters and hope-for-the-best. Today’s best practices use analytics and automation to maximize collections while maintaining positive owner relationships. Key pillars of a smart AR recovery strategy include:

1. Predictive analytics for prioritization. Not all delinquencies are equal. Analytics score accounts by likelihood of repayment, helping managers focus on the most collectible first.

2. Automated outreach. Smart systems trigger tailored, multi-channel reminders 24/7, catching delinquencies early and reducing manual effort.

3. Empathetic messaging. Communications emphasize flexibility and respect, offering payment plans and resources that resolve debts while preserving goodwill.

4. Continuous adaptation. Dashboards track response and recovery rates, enabling real-time adjustments and scaling as delinquency volumes rise.

Case Study: WRMC, Inc.

Worth Ross Management Company (WRMC) recently rolled out an AI-driven AR recovery platform. By embedding this solution, they automated the outreach to delinquent owners and resolved a large majority of outstanding balances in-house.

The result was substantial recovered revenue for their client communities and additional income for WRMC. In fact, the platform (called TechCollect) has proven capable of resolving over 70% of delinquencies before legal action is needed, which translated into roughly $2.40+ per unit of extra revenue across their managed portfolio (through retained late fees and cost savings). This real-world outcome shows the power of AR recovery: it not only helps the HOAs get paid, but also rewards the management company for facilitating the solution. Few other initiatives can so directly and positively impact the bottom line for both parties.

Secure Budget Health with Smart AR Investment

The evidence is overwhelming: economic storm clouds are gathering, and HOA/COA finances will be tested in the coming year. We see consumers weighed down by debt and slipping into delinquency on multiple fronts – credit cards, auto loans, and even mortgages. Mortgage lenders are preparing by increasing loss reserves, and foreclosure activity is ticking up again. These macro factors signal that community associations must prepare as well, because homeowner delinquencies on assessments tend to follow broader credit delinquencies.

Fortunately, management companies are not helpless bystanders. By taking decisive action now – particularly by investing in a smart AR recovery program – you can materially strengthen your community’s financial position before conditions worsen.

Budget season is the time to allocate resources to AR recovery and bake expected gains into your 2026 budget, and this can all be completed through your Exhibit B. The rationale is simple: recovering existing receivables is far less painful than imposing new charges or cutting services later.

The Contrast is Stark.

And it all hinges on decisions made now, during this “closing window” of opportunity. The tools and strategies are available – as we’ve outlined, data-driven AR recovery (with predictive analytics and automated, empathetic outreach) is a proven approach that can resolve the bulk of delinquencies efficiently. Solutions like TechCollect are ready to deploy and integrate seamlessly into existing HOA software and workflows, meaning you can start reaping results within this budget cycle. Such platforms have demonstrated measurable improvements in collection performance, often clearing the majority of past-due accounts without escalation. Investing in this capability now is akin to reinforcing your financial levees before the storm hits.

Community finances can be stabilized, but timing is critical. The economic indicators we’ve discussed serve as both warning and motivation. HOAs/COAs that seize this moment to shore up their AR will enter 2026 on much firmer footing, able to weather higher delinquency environments. Those that delay may find the window closed, with far fewer options and far tougher consequences. The message to boards and managers is clear: don’t wait until it’s too late. Leverage smart AR recovery practices today to secure your community’s budget tomorrow.

By taking action now – and using modern tools to do so – you can confidently say you’ve done everything possible to protect your community’s financial well-being. In a world of uncertainties, that proactive stance is something you’ll never regret. The window is closing, but it hasn’t shut yet – now is the time to act and ensure your community’s finances remain strong and resilient.

{kind=link}